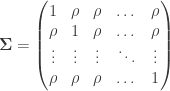

In this previous post, I introduced the concept of an equicorrelation matrix, i.e. an  matrix where the entries on the diagonal are all equal to

matrix where the entries on the diagonal are all equal to  and all off-diagonal entries are equal to some parameter

and all off-diagonal entries are equal to some parameter  which lies in

which lies in ![[-1, 1]](https://s0.wp.com/latex.php?latex=%5B-1%2C+1%5D&bg=ffffff&fg=333333&s=0&c=20201002) :

:

There, I noted that for the matrix to be positive definite, we need  . (Alternatively,

. (Alternatively,  is equivalent to

is equivalent to  being positive semidefinite.)

being positive semidefinite.)

It might seem a little strange that has a non-trivial lower bound but no non-trivial upper bound. A quick direct proof of the lower bound follows from the fact that the determinant of a positive semidefinite matrix must be non-negative. We can explicitly compute the determinant of the equicorrelation matrix, so

![\begin{aligned} 0 &\leq \text{det} ({\bf \Sigma}) = (1-\rho)^{n-1}[1 + (n-1)\rho], \\ 1 + (n-1) \rho &\geq 0, \\ \rho &\geq -\frac{1}{n-1}. \end{aligned}](https://s0.wp.com/latex.php?latex=%5Cbegin%7Baligned%7D+0+%26%5Cleq+%5Ctext%7Bdet%7D+%28%7B%5Cbf+%5CSigma%7D%29+%3D+%281-%5Crho%29%5E%7Bn-1%7D%5B1+%2B+%28n-1%29%5Crho%5D%2C+%5C%5C++1+%2B+%28n-1%29+%5Crho+%26%5Cgeq+0%2C+%5C%5C++%5Crho+%26%5Cgeq+-%5Cfrac%7B1%7D%7Bn-1%7D.+%5Cend%7Baligned%7D&bg=ffffff&fg=333333&s=0&c=20201002)

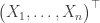

Here’s another proof of the lower bound that might be slightly more illuminating. Recall that being (symmetic) positive semidefinite is equivalent to the existence of random variables  such that the random vector

such that the random vector  has covariance matrix . Hence,

has covariance matrix . Hence,

Now for some intuition. When  , the lower bound is the trivial

, the lower bound is the trivial  , which can be achieved when

, which can be achieved when  . Now, imagine that

. Now, imagine that  : how can we add

: how can we add  so that the pairwise correlations are minimized (i.e. be most negative)? There is an inherent tension: the more negatively correlated we make with

so that the pairwise correlations are minimized (i.e. be most negative)? There is an inherent tension: the more negatively correlated we make with  , the more positively correlated becomes with

, the more positively correlated becomes with  . So there is no way for

. So there is no way for  for every pair

for every pair  .

.

One analogy that could be helpful is to think of each  as a magnet that only repels, and we are trying to squeeze all the magnets into one box. As we add more and more magnets, the magnets get closer and closer together (even though they are still trying to repel each other). We don’t get the same problem with magnets that only attract: they all simply stick to each other at a single point, no matter how many magnets we add.

as a magnet that only repels, and we are trying to squeeze all the magnets into one box. As we add more and more magnets, the magnets get closer and closer together (even though they are still trying to repel each other). We don’t get the same problem with magnets that only attract: they all simply stick to each other at a single point, no matter how many magnets we add.

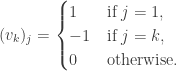

, where

, where  is the column vector with all entries being 1 and

is the column vector with all entries being 1 and  is the identity matrix.

is the identity matrix. , with associated eigenvector

, with associated eigenvector  . The second eigenvalue is

. The second eigenvalue is  , with

, with  associated eigenvectors

associated eigenvectors  , where the entries of

, where the entries of  are

are This can be verified directly by doing the matrix multiplication.

This can be verified directly by doing the matrix multiplication.![\text{det} ({\bf \Sigma}) = (1-\rho)^{n-1}[1 + (n-1)\rho]](https://s0.wp.com/latex.php?latex=%5Ctext%7Bdet%7D+%28%7B%5Cbf+%5CSigma%7D%29+%3D+%281-%5Crho%29%5E%7Bn-1%7D%5B1+%2B+%28n-1%29%5Crho%5D&bg=ffffff&fg=333333&s=0&c=20201002) . This is because the determinant of a square matrix is equal to the product of its eigenvalues.

. This is because the determinant of a square matrix is equal to the product of its eigenvalues. . This can be verified directly by matrix multiplication. It can also be derived using the

. This can be verified directly by matrix multiplication. It can also be derived using the