Value at Risk (VaR) is an important concept in finance and risk management that quantifies the risk on an investment or portfolio.

To define VaR, we need to fix two things: (i) the time horizon, and (ii) the probability of loss. For a time horizon

Over the time horizon

Riskier investments will tend to have higher VaR.

Sometimes, instead of defining the probability of loss

The VaR of this investment at level

Larger values of

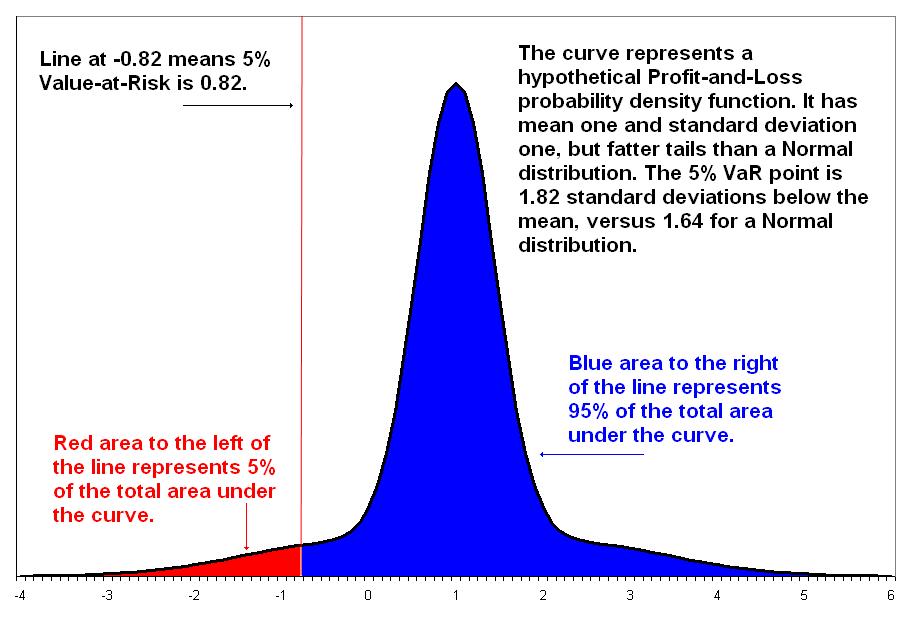

The following diagram (taken from the Wikipedia article, Reference 1) illustrates how VaR relates to the probability distribution of investment value at the end of the time horizon. For 5% VaR (or equivalently VaR at level 0.95), we find the x-value such that the area under the curve on the left is exactly 5%. Since the distribution is depicting possible profits (larger values are better), 5% VaR would be the negative of the cutoff: Over the time horizon, there is a 5% probability that we will lose 0.82 or more.

Mathematically, VaR is simply a quantile of the appropriate distribution. If

Mathematically, VaR is simply a quantile of the appropriate distribution. If

There are several ways to compute/estimate VaR, see for e.g. Reference 2 from Investopedia.

References:

- Wikipedia. Value at risk.

- Investopedia. What is Value at Risk (VaR) and How to Calculate It?

Pingback: What is Conditional Value at Risk (CVaR)? | Statistical Odds & Ends

Pingback: CVaR and a lemma from Rockafellar & Uryasev | Statistical Odds & Ends